A decisioning engine is smart software that automates complex decisions by analyzing data against set rules to deliver accurate results. In lending, decisioning engines serve as the foundation of modern credit operations, determining whether to approve or decline a loan application.

By embedding intelligence into credit workflows, lenders can scale, innovate with confidence, and respond to changing market conditions.

As the lending system is being formed by automation and artificial intelligence, decisioning engines are changing how lenders operate and deliver value to their customers.

How decisioning engines work in lending

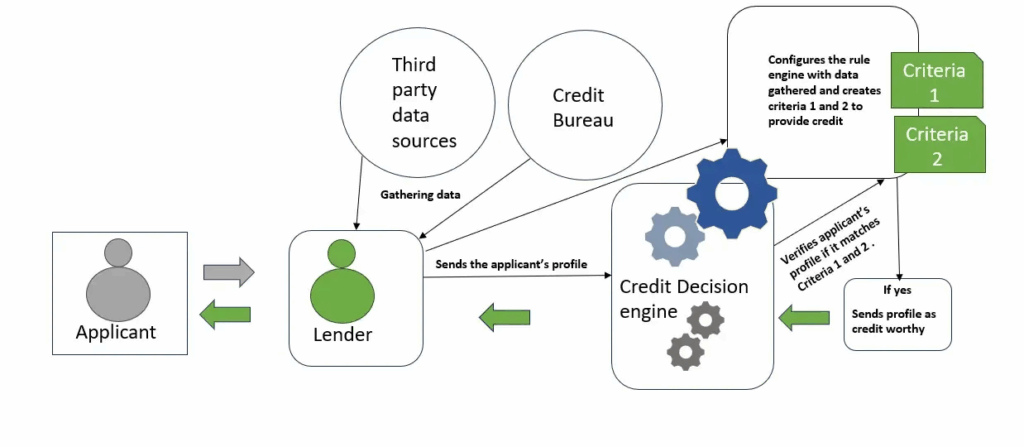

A decisioning engine serves as the central hub for loan origination. The process is sequential and designed to handle accuracy and risk management.

Once a borrower submits an application and relevant data is collected, the engine applies multiple layers of evaluation to reach a final decision.

Knockout rules: The first layer applies knockout rules, filtering out applicants who fail to meet basic eligibility criteria. These rules include minimum age, residency, income thresholds, and other regulatory requirements. By eliminating ineligible applications, lenders save time and operational resources. This ensures that underwriters focus on candidates with potential.

Data enrichment: After initial filtering, the engine enriches application data with external sources. This can include credit bureau reports, fraud-detection databases, employment verification, and alternative data sources. By integrating these third-party inputs, the system confirms the accuracy of applicant information and provides insight into potential risks.

Risk scoring and predictive modeling: Next, the engine applies risk scoring and predictive analytics. Leveraging artificial intelligence and machine learning, it assesses an applicant’s repayment likelihood and identifies delinquencies. The models can adapt, learning from new repayment patterns and historical trends.

Affordability and portfolio alignment: The engine assesses how a potential loan aligns with the lender’s portfolio strategy. It checks whether the loan amount, term, and interest rate align with the organization’s risk appetite and diversification goals.

Manual review when needed: Some applications require human judgment. High-value loans, borderline cases, or applications with unusual data patterns may be flagged for manual review. This layered approach ensures that automated efficiency does not come at the expense of nuanced decision-making or regulatory compliance.

Decisioning engines have come up as a solution to competing demands, providing a framework that automates, standardizes, and accelerates loan decision-making. Here are some reasons why it matters:

Accelerating processing times

Decisioning engines simplify every stage of loan assessment, from verifying borrower details to calculating risk, completing processes in minutes that would take hours.

By eliminating manual tasks, lenders can respond to borrower applications almost instantly, reducing dropout rates. In a market where 75% of borrowers expect near-instant loan decisions, speed impacts conversion and retention.

Reducing costs

Centralized automation reduces dependency on disparate systems and lowers human resource requirements. Few manual checks mean skilled staff can focus on exceptions and strategic analysis rather than repetitive tasks.

According to industry studies, automating decision workflows can cut operational costs by up to 30% while reducing errors that would result in remediation.

Ensuring compliance and transparency

Regulatory compliance in lending is complex, covering KYC, AML, fair lending, and data protection standards.

Decisioning engines embed compliance rules into automated workflows, ensuring every decision is traceable and auditable.

This reduces the chances of regulatory breaches and fines. Transparency also benefits borrowers: they can be confident that lending decisions are fair, standardized, and free from arbitrary judgment.

Enhancing adaptability

Financial markets are dynamic, and credit risk models or lending criteria need to be adjusted. Decisioning engines allow lenders to modify rules, integrate new data sources, or adapt predictive models.

Lenders can respond to market dynamics, competitor strategies, or developing borrower trends.

Improving risk management

Manual or fragmented decision-making introduces inconsistencies and increases the risk of defaults or non-compliance.

Decisioning engines use AI and predictive analytics to assess risk, identify potential delinquencies, and flag suspicious behavior. Continuous monitoring of portfolio performance enables proactive risk mitigation.

Enabling data-driven insights

Beyond processing loans, decisioning engines generate valuable analytics that inform strategy. Lenders gain insight into borrower behavior, portfolio performance, approval trends, and risk concentrations.

These insights enable more informed decision-making, targeted marketing, and refined product offerings.

Today, modern decisioning engines powered by AI and ML are used to adapt to data and deliver informed lending decisions.

Unlike static credit models that apply uniform formulas to every applicant, AI-driven decisioning engines learn from each new application and repayment cycle.

They identify trends in income stability, spending patterns, and alternative data sources to refine credit risk predictions.

This dynamic risk assessment enables fair evaluations, especially for first-time borrowers who might otherwise be excluded from credit access.

By analyzing detailed customer profiles, decision engines can recommend customized loan products that reflect each individual’s borrowing capacity.

This could mean flexible repayment tenures, adaptive interest rates, or credit limits that scale with income trends.

Instead of waiting for defaults to occur, the system can detect early warning signs such as irregular deposits or missed payments. These indicators trigger alerts, allowing lenders to adjust loan terms or offer support before risks escalate.

The most transformative feature of AI-powered decisioning is its ability to operate in real time. These systems can process large volumes of data and deliver loan decisions within seconds. This immediacy meets borrower expectations for transparent lending experiences.

In essence, integrating AI and machine learning transforms lending from a rule-bound, reactive process into a proactive, intelligence-driven strategy.

Practical applications beyond lending

While lending is where decisioning engines have gained the most traction, their usefulness extends far beyond finance. Any industry that relies on fast, consistent, and data-driven decision-making can benefit from this technology.

Telecommunications: Providers use decisioning engines to design promotional offers, adjust data plans by predicting when customers are likely to switch providers.

Retail: Dynamic pricing models powered by decisioning engines adjust product prices based on demand, seasonality, or customer loyalty levels.

Insurance: Underwriting decisions and claims assessments are automated using risk models that factor in real-time data such as driver behavior, location, or health metrics.

Manufacturing: Predictive maintenance systems use decision logic to schedule equipment maintenance before failures occur.

Healthcare: Decisioning engines assist in diagnostics and treatment planning by analyzing patient data, medical histories, and response patterns, helping practitioners make evidence-based recommendations.

Selecting the right decisioning engine determines how efficiently a lender operates. A strong decisioning engine begins with robust integration capabilities.

It should connect to core banking systems, credit bureaus, payment providers, and third-party APIs to pull in real-time data for decision-making. Fragmented integrations create data silos that weaken risk insight.

Lenders should be able to modify or add decision rules without relying on IT teams. This flexibility allows credit and business teams to respond to changes in market behavior.

A no-code or low-code interface is valuable here, empowering non-technical staff to manage complex logic.

Given the regulatory pressure in financial services, compliance support must be built in from the ground up. The ideal engine provides decision explainability and automated checks that align with frameworks. Transparent documentation of how each decision was made satisfies auditors and enhances lenders’ trust.

Modern platforms should also incorporate AI and analytics support that refines credit scoring to analytics dashboards that help teams track performance in real time.

Finally, scalability and performance determine how well the system can grow with the business. As you develop new product lines, the engine should maintain speed and precision. Low latency and high reliability ensure consistent decision quality.

The future of lending belongs to those who can make intelligent decisions at scale. Decisioning engines are the competitive advantage that separates market leaders from those struggling to keep up.

By automating complex evaluations, these systems enable lenders to deliver the experiences borrowers demand.

But transformation doesn’t require building everything from scratch. The right decisioning infrastructure should eliminate the need to build lending and underwriting logic from scratch.

Need guidance on decisioning? Adjutor, Lendsqr’s next-generation decisioning engine, was created to help lenders automate credit decisions. Explore adjutor’s decisioning APIs and see how custom scoring models can fit your lending strategy

If you’re a non-profit or development finance institution (DFI), it should be easier to run a lending program if you're already doing the hard part of reaching people most others won’t.

So what is Lendsqr, and how does it work? What makes Lendsqr the go-to platform for lending? Explore its key features and how they can help you build a thriving loan business.

The end-to-end loan management software that’s rewriting the rules for lenders globally by offering enterprise-grade features without the enterprise-grade costs.