Categories of low-risk borrowers lenders should target

Back

Information

Categories of low-risk borrowers lenders should target

Last updated May 24, 2026

Eseose Animhiaga

In this post

Share

Knowing who to lend to is the holy grail of lending, which the credit alchemists have been battling for centuries. This could also mean that expanding your loan business often means extending credits to higher-risk borrowers.

But what if you prefer a more cautious approach, targeting lower-risk groups? As you craft your business model and plan, one question commonly crops up – do you want to cater to a broad audience or niche down?

Often, when lenders express a reluctance to lend to high-risk borrowers or a desire to avoid the mass market, it raises the question – who exactly are the low-risk customers they seek? Saying, “I don’t want high-risk borrowers,” is one thing; articulating the low-risk customers you seek is another. These categories of traditionally low-risk borrowers exist; we have done the grunt work of identifying and categorizing 5 of these customers.

These borrowers fall into the category of those with verifiable businesses. You can clearly understand their activities, cash flow, and repayment plans. Typically, they operate from physical offices, making on-site assessments and creditworthiness verification feasible. The likelihood of them disappearing without a trace is minimal, resulting in a lower risk level. Their well-established business history often translates to a reliable financial track record, contributing an extra layer of trustworthiness. Plus, physically seeing how they operate gives you a good sense of their financial situation.

Women traders (AKA market women)

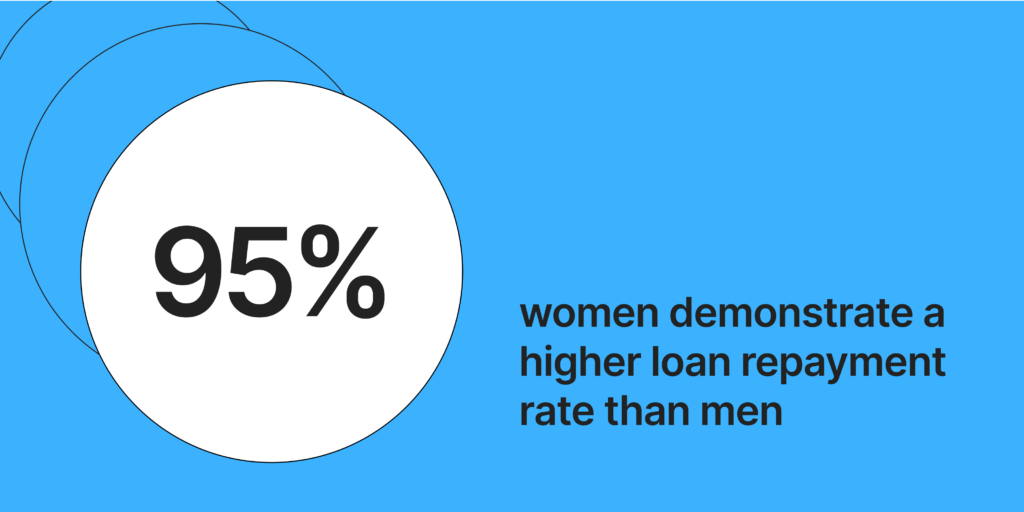

Data insights from Zimbabwe Women’s Microfinance Bank

The Zimbabwe Women’s Microfinance Bank found that women demonstrate a higher loan repayment rate than men. Women traders, particularly those engaged in small to medium-scale businesses, are known for their prudent financial habits and adherence to the law, contributing to their reliability. Many of them operate physical shops, providing tangible assets for assessment. It’s important to note that these traders, though distinct from formal SMEs, often operate as sole proprietors with less formal business structures. This distinction suggests they may benefit from tailored loan offers and terms that suit their unique circumstances. See how one of our lenders currently serves this category of borrowers.

Government employees

An illustration of a Government employee

Government employees represent a low-risk category for lenders. Their consistent salary payments and contractual commitment to uphold their organization’s reputation make them cautious borrowers, avoiding any embarrassment. With job security, they become even more reliable borrowers. The chances of them defaulting on loans are low since they are unlikely to quit their jobs voluntarily. This blend of financial stability and professional dedication positions government workers as a highly reliable category of low-risk borrowers for digital lenders.

Collective unions

An illustration of a group of people forming a trade union

Groups like drivers’ and traders’ unions are another set of low-risk borrowers. These groups often practice in-house small-scale peer-to-peer lending. In Yoruba, Nigeria, they call them Alajo. Collective unions can be guarantors for members seeking loans, with defaulters facing consequences and potential ostracization. This discourages members from defaulting due to the fear of being shunned and dismissed. The shared sense of community and mutual trust within these groups fosters a supportive environment for financial transactions like lending to thrive and lowers the chance of missed payments.

Read more

Working class (Professionals)

An illustration of a Doctor

For professionals like Teachers, Doctors, Nurses, Lawyers etc, their profession is more than just a job to them. Their professional ethics and oaths bind them to remain law-abiding citizens or risk losing their practice license. This commitment and adherence to a strict moral code make them reliable borrowers likely to respect the terms and conditions of their loans.

One thing in common with all five (5) groups listed above is CONSEQUENCES. Therefore, we agree that the key to discovering low-risk borrowers lies in targeting individuals within settings that enforce severe consequences for bad behavior and misconduct. Let’s hear from you. What are your questions or experiences with lending so far? Send us a message at [email protected].

You need the right technology for lending success

We’re in the business of helping lenders worldwide have access to the best technology, and use credit to lift billions to their dreams and a better life.

If you’re a non-profit or development finance institution (DFI), it should be easier to run a lending program if you're already doing the hard part of reaching people most others won’t.

So what is Lendsqr, and how does it work? What makes Lendsqr the go-to platform for lending? Explore its key features and how they can help you build a thriving loan business.

The end-to-end loan management software that’s rewriting the rules for lenders globally by offering enterprise-grade features without the enterprise-grade costs.