It’s a widely spread belief amongst lenders that handing over cash or processing loans faster is all that borrowers want. Unfortunately, lending is more nuanced than this. To have a deeper understanding into what drives Nigerians towards one lender or the other, Lendsqr conducted a survey to find out the preferences of borrowers in Nigeria.

This article details the insights drawn from the results of our survey regarding the deciding factors for borrowers when selecting a lender.

We asked a series of questions to establish the desires of borrowers from lenders – what their pain-points are, features they want to see, moments of delight in their journey and other aspects that make up their typical borrowers’ journey.

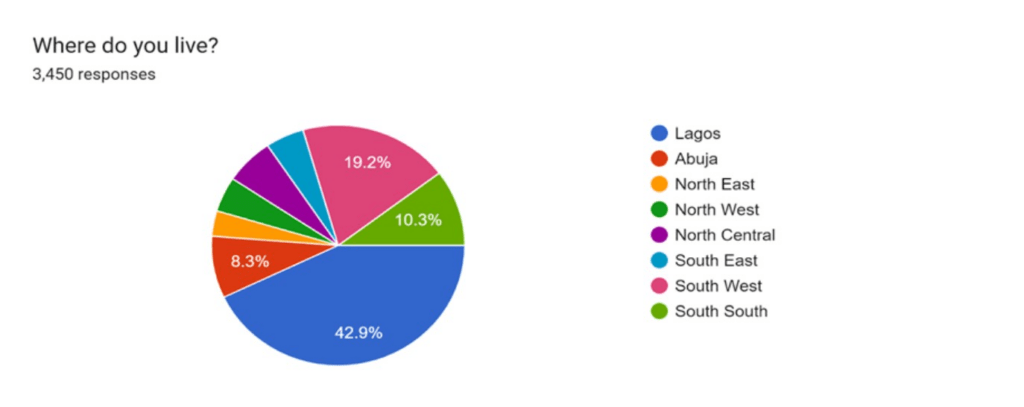

The survey was digitally deployed to over 3,000 respondents across Nigeria. About 60% of the respondents are based in Lagos and other south-western states, while roughly 20% of respondents are based in Abuja and other northern states.

Based on our findings, we explore some of the top things borrowers want from lenders below:

Reasonable interest rates

These days, the average lender charges between 48% to 120% interest per annum on loans. These rates can really put a dent in borrowers’ finances and adversely affect their ability to repay these loans. Our position remains that credit should be affordable and sustainable. Our survey results reveal that borrowers agree with us.

Borrowers want to be charged reasonably on the loans they take from lenders. They don’t want repaying a loan to leave them in worse financial shape than they were before taking the loan. More often than not, higher interest rates are a lenders’ attempt to cover the costs of lending.

Fortunately, lenders can reduce their cost of lending with Lendsqr’s technology-driven lending solutions that support lenders to lend profitably at scale. You can reach out to [email protected] for more information on how Lendsqr can help you reduce your cost of lending.

Digital-led onboarding experience

A digital-led onboarding experience is driven by the product itself. This means the onboarding process is low-touch and requires little to no human interaction for borrowers to sign up and start their borrowing experience with you.

Alternatively, agent-led onboarding relies heavily on human interaction to convert borrowers and guide them through the onboarding process. It’s very high-touch and personal and usually involves phone calls or live chat between agents and customers.

Borrowers showed a greater affinity with digital interactions and established their preference for a digital-led onboarding experience over agent-led onboarding.

Digital-led onboarding experiences ranked significantly higher than agent-led onboarding experiences with a positive variance of 13%. These results show that borrowers, who often approach lenders for urgent cash needs, would rather not be burdened with relying on human interaction to complete their signup process.

Lenders stand to benefit from implementing a seamless, low-touch in-app onboarding process for borrowers.

Data privacy/security

Respondents also answered that data privacy/security concerns influence their choice of lender. Borrowers entrust lenders with access to sensitive financial data and other confidential data during the loan process. It’s expected that lenders don’t misuse this data outside of the provisions of the Nigeria Data Protection Regulation (NDPR) at the detriment of customers.

Unfortunately, this breach of customers’ data privacy is often associated with unethical and bad attempts at recovering loans. Recovering loans isn’t the easiest task, however, borrowers’ rights to data privacy is non-negotiable.

You can’t have a lending business without borrowers. Borrowers are your customers and it’s important to keep them happy and ensure they have the best possible experience (within reasonable boundaries) interacting with your business.

Borrowers look out for lenders with a speedy and seamless loan process. Borrowers are more likely to rely on lenders who can cater to their credit needs as quickly as possible.

18% of respondents highlighted the presence of financial coaching as a deciding factor for them in selecting a lender. With the increasing ease of accessing credit for the everyday Nigerian, borrowers may approach financial offers with caution.

Borrowers look to the professionals for expert financial advice on credit and general money-related issues. Borrowers may generally feel more comfortable with lenders who help them understand the finance jargon that accompanies loan offers.

This is even more relevant to abate borrowers’ fear about the possibility of you being a loan shark. A lack of understanding poses a major barrier to borrowing responsibly.

There’s room for improvement in financial literacy in Nigeria. Lenders can invest in efforts to make learning resources available for borrowers. This can be in the form of a blog, social media posts, email blasts, etc. These can be frequently updated with informative and relatable content for the average Nigerian borrower.

Loans via mobile apps

As a lender looking to grow your lending business successfully, it’s important to know where to play to win. 76% of respondents stated mobile apps as their preferred channel for taking out loans. This was followed by website applications, a branch (physical office) and agents at 13%, 8% and 3% respectively.

The overwhelming preference for digital channels positions them as priority for lenders in engaging their customers. It’s widely known that building a mobile application for your lending business is expensive.

However, you can get your own lending mobile application with Lendsqr at a fraction of the cost of your own proprietary building efforts. Furthermore, you can dominate the digital space and cater to borrowers where they’re most comfortable.

The introduction of more structured and formal avenues of financing have not replaced informal savings and financing schemes for 40% of our respondents.

These respondents reported that they participate in some form of informal money savings scheme. This highlights that despite the growth in the number of digital savings companies, thrift savings remain a strong option for Nigerians.

Opportunities exist for lenders to partner with thrift lending associations to increase their market reach. This could be done by setting up a peer-to-peer lending feature on your lending application for informal lenders to sign-up to digitally deliver their lending products.

Giving borrowers what they want can be expensive and difficult. But not if you lend with Lendsqr. You can sign up for free and start making smarter lending decisions to deliver the best possible experience to your borrowers.

Obtaining an FCA consumer credit license is a key step for businesses that want to offer loans, credit cards, BNPL, or other consumer credit products in the UK. This guide explains who needs FCA authorization, the application process, eligibility requirements, expected costs, and practical tips to help lenders navigate the licensing process successfully.

If you’re a non-profit or development finance institution (DFI), it should be easier to run a lending program if you're already doing the hard part of reaching people most others won’t.

The end-to-end loan management software that’s rewriting the rules for lenders globally by offering enterprise-grade features without the enterprise-grade costs.