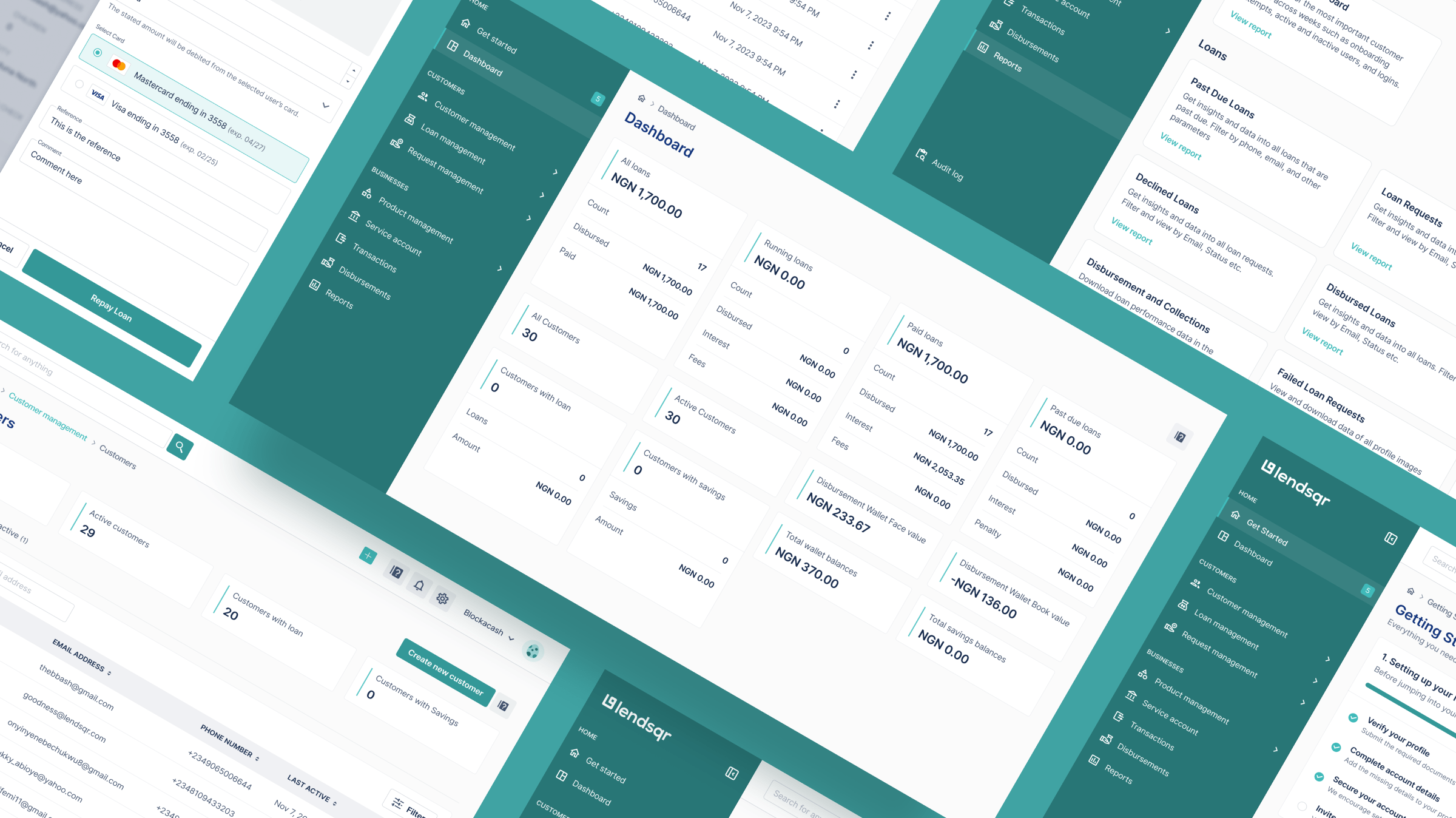

Industry Information

How to start a lending business in Nigeria

This guide walks through the practical steps you need to take to start a lending business in Nigeria.

🎥 You can now request videos during loan applications

Hello, and Happy New Month! 🎉 Welcome to October! To our Nigerian lenders, we extend our warmest congratulations on celebrating Independence Day 🇳🇬. As we enter the final quarter of the year, it’s time to reflect on the goals you set for your lending business at the start of 2024. Whether you’ve met them or […]

FAQs

Requirements for publishing Nigerian loan apps on Apple App Store

The big question is: where’s the best place to launch your loan app to reach the most users? Let's take a closer look at the one of them - Apple App Store.