Let’s help you separate sheep from wolves!

We both know that not all customers are the same: some are angels, others are less salubrious; some are good for the money, and others will probably fleece you. How then do you separate the wheat from chaff or the sheep from the wolves? Or how do you even meet regulatory demands of Know Your Customer (KYC) where customers should be tiered based on what you know about them and the documents they have provided to you?

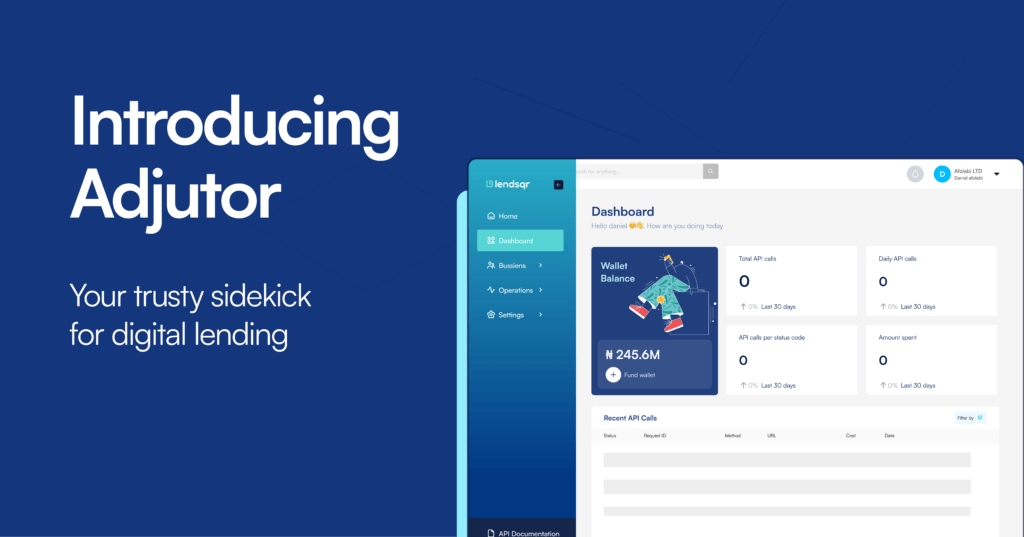

Meet Adjutor: Your critical support for making better credit decisions

Making the right credit decisions requires more than instinct, it demands access to reliable data, clear insights, and the right tools. Adjutor is designed to support lenders at this critical point, helping them assess risk, evaluate borrowers more accurately, and make smarter, faster decisions. By providing deeper visibility into credit behavior and simplifying complex data, Adjutor empowers lenders to reduce risk while maintaining efficiency and growth.

Reach more customers with the Lendsqr offline loan feature

As a digital lender, there are so many things to consider when creating your loan portfolio. How do you create the perfect products that would reach your ideal target customer? What if your target customer base may not be tech-savvy or does not have access to the internet at all? How do you cater to […]

How the Lendsqr Karma service blocks bad actors and defaulters

Lending becomes harder when the same bad actors move across platforms, taking loans with no intention to repay. This is where Lendsqr’s Karma service comes in. By checking borrower identities, device patterns, and past behavior across the ecosystem, Karma helps lenders identify defaulters and fraud risks early in the decision process. This article explains how it works and how it helps protect loan portfolios from repeat abuse.

A1 Credit: Using digital channels to give loans to Nigerians and SMEs

A1 Credit is part of a growing shift in Nigeria’s lending space, where digital channels are being used to reach individuals and small businesses that traditional systems often overlook. By moving loan applications, verification, and disbursement online, lenders can respond faster to demand while working with limited credit histories and informal income patterns. This article looks at how A1 Credit approaches digital lending, the role of alternative data and automated decisioning, and what this means for Nigerians and SMEs seeking more accessible and responsive financing options.

How to design a customer centric lending product

A good product is one which fits and addresses specific needs of the market. It’s almost impossible to gain market share or domination without tailoring one’s offerings to the needs of customers.

Preparing your income statement as a lender- management accounting 101

Preparing an income statement as a lender goes beyond simple bookkeeping, it is a critical tool for understanding profitability, tracking performance, and making informed decisions. From interest income and fee revenue to loan losses and operating expenses, every line tells a story about how your lending business is performing. For lenders, especially those still building structure, getting this right is essential to managing risk, ensuring sustainability, and gaining clear visibility into where the business is truly making or losing money.

Drafting a strategy for your lending business

Drafting a strategy for your lending business requires more than setting growth targets, it involves making clear decisions about your market, risk appetite, product structure, and operational model. From defining your ideal borrower to aligning your credit policies and funding approach, every element must work together to support sustainable growth. A well-thought-out strategy not only guides day-to-day decisions but also helps lenders stay resilient in the face of changing market conditions and borrower behavior.

How to grow your customer base as a lender

Growing your customer base as a lender requires more than just offering loans. It’s about understanding your market, building trust, leveraging digital channels, and creating experiences that keep borrowers coming back. This guide explores actionable strategies to attract and retain clients effectively.

Device finance in Nigeria: A case for BNPL

In an era where a smartphone is no longer a luxury but a fundamental tool for economic survival, Nigeria's "affordability gap" has never been wider. With inflation squeezing disposable income, the traditional model of outright cash purchases is being replaced by the rapid rise of Buy Now, Pay Later (BNPL). This shift isn't just about convenience; it’s a strategic response to currency volatility and a lack of traditional credit infrastructure. By leveraging alternative data and "pay-as-you-go" technology, BNPL providers are turning the dream of high-end tech ownership into a manageable monthly reality for millions of Nigerians, ultimately driving the nation's next wave of digital inclusion

APIs for lenders to reduce NPL

Integrations via API to other ancillary platforms are key to ensuring your loans are paid back. They allow you to leverage on the tech, data and functionalities of the best providers to improve the quality of your loan flow.