How to use Route Mobile with Lendsqr for sending SMS

Once you have your Route Mobile API key, log in to your Lendsqr account. Reach out to our product support team at [email protected] and get set up in 10 minutes.

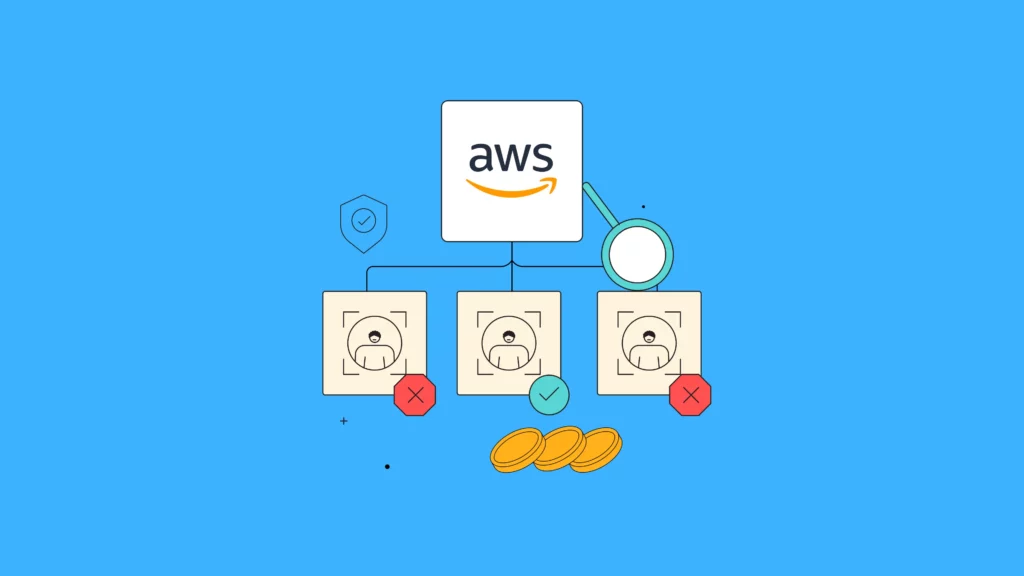

How we used AWS to build our identity and liveness system

Building reliable identity verification and liveness detection systems is one of the biggest challenges facing modern digital platforms, especially in fintech, lending, and online onboarding. These systems must balance speed, accuracy, scalability, fraud prevention, and user experience, all while handling large volumes of sensitive customer data securely. In this article, we explore how we used Amazon Web Services (AWS) to build our identity and liveness system, covering the infrastructure choices, architecture decisions, verification workflows, and AWS services that powered the solution. From facial recognition and document verification to scalability, security, and real-time processing, this piece breaks down the practical lessons, challenges, and technical considerations involved in developing a robust digital identity system.

5 types of lending model

Lending is not a one-size-fits-all business. Different lenders operate with different structures, risk models, customer segments, and repayment approaches depending on their market and goals. Understanding the various lending models is important for choosing the right strategy, technology, and operational process for sustainable growth. In this article, we explore five common types of lending models, how they work, and the kinds of borrowers and institutions they are best suited for.

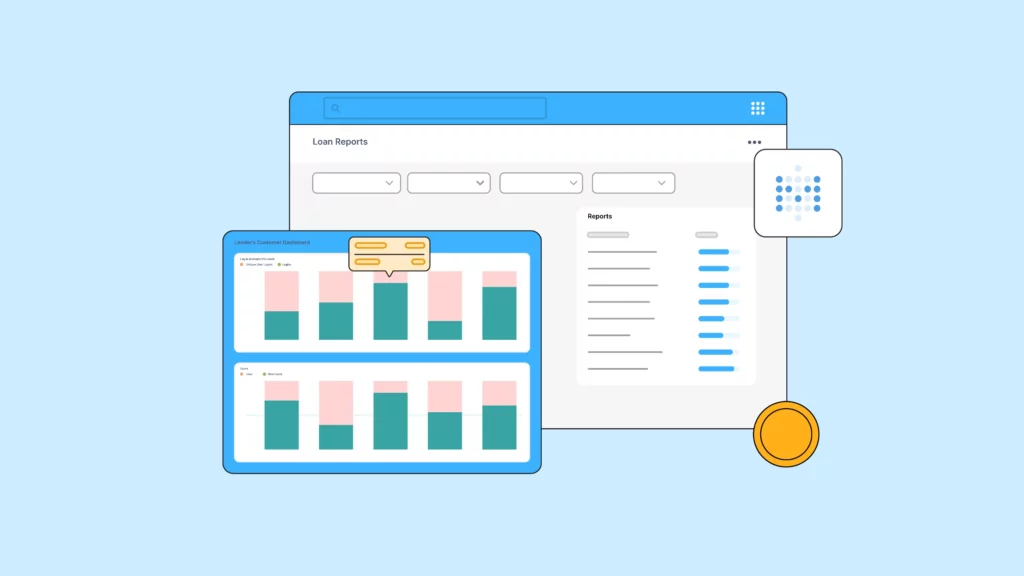

How we use Metabase to power our internal reporting

Data-driven decision-making is critical for modern teams, but building reliable internal reporting systems can quickly become complex without the right tools. From tracking operational performance to monitoring customer activity and business growth, organizations need reporting systems that are flexible, accessible, and easy to scale across teams. In this article, we explore how we use Metabase to power our internal reporting, including how we structure dashboards, monitor key metrics, automate reporting workflows, and make business data more accessible across the organization.

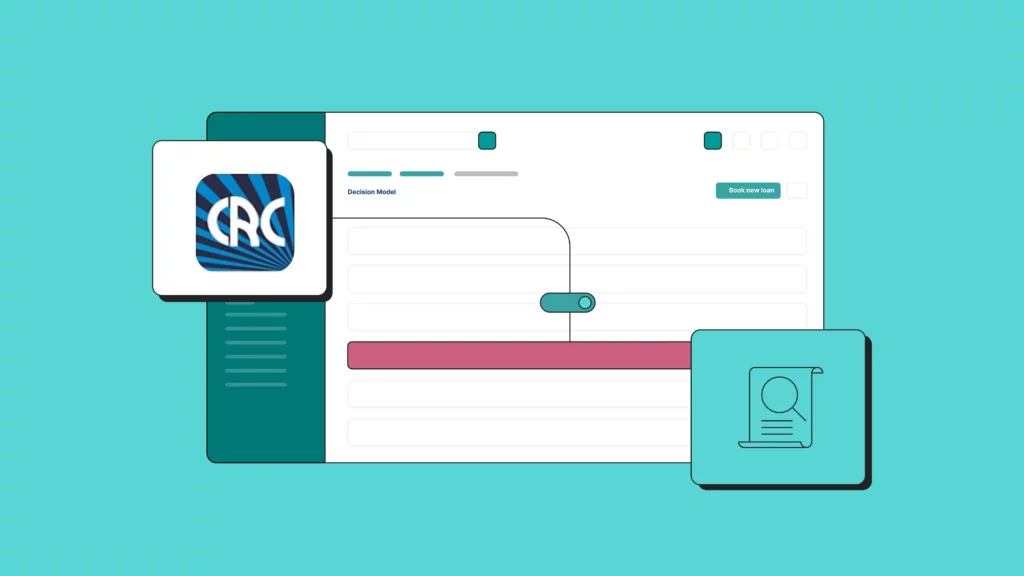

How to set up CRC Credit Bureau for Lendsqr

Integrating CRC Credit Bureau with Lendsqr helps lenders make faster and more informed credit decisions by giving them access to borrower credit history directly within their lending workflow. This guide walks through the setup process step by step, from obtaining your CRC credentials to configuring the integration on Lendsqr. Whether you are onboarding a new lending operation or improving an existing credit process, setting up CRC correctly can help reduce risk, strengthen underwriting, and improve overall loan performance.

How we built our URL shortener (Monstrator) as a replacement for Bitly

Monstrator is Lendsqr’s in-house URL shortener built as a scalable replacement for Bitly, designed to give us full control over link tracking, reliability, and performance across our marketing and product communications. In this article, we break down why we moved away from third-party tools, the architecture behind Monstrator, and how it was engineered to handle high-volume link generation while providing accurate analytics and seamless integration across our ecosystem.

How to use Infobip with Lendsqr as an SMS provider

Integrating Infobip with Lendsqr allows lenders to automate and manage SMS communication across the entire lending journey, from OTP verification and loan application updates to repayment reminders and collections messaging. This guide walks through how to connect Infobip as your SMS provider on Lendsqr, configure messaging settings, and ensure reliable delivery for customer notifications at scale.

How to use Loandisk with Lendsqr

LoanDisk helps lenders manage borrowers, loans, repayments, and customer records, while Lendsqr provides a broader lending infrastructure that supports loan origination, underwriting, collections, and automation. This guide explains how to use LoanDisk alongside Lendsqr, covering integration options, workflow considerations, data synchronization, and best practices for creating a more efficient lending operation across customer onboarding, loan management, and repayment tracking.

Indicina vs Lendsqr: Which loan management platform suits your needs?

Choosing the right lending platform can significantly impact your ability to scale, automate operations, and manage risk effectively. While Indicina is known for its credit decisioning and financial data infrastructure, Lendsqr offers a broader end-to-end lending platform covering loan origination, underwriting, disbursement, collections, and borrower management. In this article, we compare Indicina and Lendsqr across key areas such as functionality, integrations, automation, scalability, and use cases to help you determine which platform best fits your lending business.

7 effective debt collection practices and legal considerations

Effective debt collection is about more than recovering overdue payments—it also requires maintaining compliance, protecting customer relationships, and reducing legal risk. Lenders must balance persistence with professionalism while adhering to applicable laws and regulations governing collections activities. In this article, we explore seven effective debt collection practices, along with key legal considerations that can help lenders improve recovery rates while operating ethically and compliantly.

What payment gateways are available to Lendsqr lenders?

Payment gateways play a critical role in the lending process, enabling lenders to collect repayments, process disbursements, manage direct debits, and facilitate seamless borrower transactions. Lendsqr supports integrations with a range of payment providers to help lenders operate efficiently across different markets and payment channels. In this article, we explore the payment gateways available to Lendsqr lenders, their key features, and how to choose the right option for your lending business.